tl;dr: Burrito bonds represent finance doing what it does best: unbundling risk, pricing it granularly, and allocating capital more efficiently. BNPL unbundles consumer credit into tradeable assets to let the market decide who should hold the risk. The result is lower borrowing costs, and a credit market that’s more effective than the status quo.

Despite skepticism from Volcker and Buffet, financial innovation has been and will continue to be a massive net positive for humanity. I will write a separate, longer piece on why financial engineering is good akshually. For now, I’ll describe why the development of the BNPL1 securities market will improve the current state of credit and lending. It’s a win-win-win-win-win. We're gonna win so much, you may even get tired of winning.

In March 2025, DoorDash and Klarna announced a deal to let consumers pay for restaurant food, groceries and other delivery orders in four equal, interest-free installments, or “at a more convenient time, such as a date that aligns with their paycheck schedules”. The commentary and memes about “burrito bonds” and Shake Shack securitization were funny. Most takes implied or directly stated it was a manifestation of late-stage capitalism. In 1983, people lamented that one had to use a “credit” card at Burger King. On some level, payments and credit are on the same spectrum of value transfer.

To take a few steps back, why does credit exist at all? One reason is that someone’s or a company’s income doesn’t always align perfectly with when they want to buy things. Credit bridges this gap by allowing the borrower to purchase now and the lender to be repaid later, with the lender earning compensation for the time value of money, repayment risk, and liquidity risks. This logic doesn’t change just because the thing being financed is a burrito.

Is financing your lunch a sign of societal decay? Maybe, maybe not. But it’s definitely an evolution in Market Completion. As a financial engineering and market completion enjoyer, I think this is great. A Complete Market is one where every risk can be priced, traded, or hedged. i.e. every risk has a price, every future has a counterparty. If you think the price of oil will be $120 after a year, you can use futures or options on futures to make this bet2. If you think the S&P 500 will be over 6,500 within 2 years and the yield on 10Y Treasury bonds will be 4.25%, investment bankers will help you express this view for a fee.

Small, short-term loans provided by BNPL providers (Klarna, Affirm, etc.) get bundled together as financial instruments and are sold to investors looking for yield. This is called securitization. This does a few useful things for the different parties involved:

For Borrowers: A simple, often zero-interest way to smooth out small expenses, if they pay on time. This contrasts with credit cards, where average rates are 15-30%, and even super-prime borrowers have a 7.22% spread (if the Fed Funds rate is 4% and the credit card APR is 10%, the spread is 6%) over the Fed Funds rate. Additionally, consumers have to only forecast the next six weeks of their life, something even people with high time preference can handle (I think).

For Restaurants/Merchants: BNPL fees (2-6%) are higher than credit card fees (1.5-3.5%), reducing the merchant’s net payout per transaction but BNPL drives higher sales volumes, offsetting the fee impact. BNPL boosts conversion, order sizes, and frequency (what else is left for a marketer to do?). So BNPL is really a customer acquisition and loyalty play funded by the merchant, not the Consumer. With BNPL, merchants do not have customer default risk since the provider pays upfront and manages collections. Unlike credit cards, where chargebacks from fraud or disputes can delay or reverse payments weeks or months later, BNPL offers merchants predictable, risk-free payouts.

BNPL Provider: The BNPL provider finances the $100 loan using its own funds, a bank credit line, or investor-backed warehouse financing.

BNPL Economics: The BNPL provider pays the merchant $95 (after a $5 fee) and collects $100 from the customer over time, earning the $5 fee as revenue. To free up capital, the provider bundles many $100 loans and sells them to investors for 95 cents on the dollar through securitization. This allows the provider to recycle funds into new loans, continuing to earn fees. To align interests with investors, the provider retains a ‘first-loss’ portion of the securitized loans, so BNPL providers have skin in the game to ensure responsible lending. After paying $0.57 for capital costs and operations, the provider’s net profit per $100 loan is $4.43. The more $100 loans they can make and get off their balance sheet, the more profits they make.

For Banks & Investors: It creates a new, short-duration segment within the Asset-Backed Securities market. BNPL loans are 6-8 weeks long. That’s a tight risk-feedback loop. In exchange for fees, banks structure these loans and quickly move them off their balance sheets and to investors. This is one of the primary roles of finance–to transfer risk to those who are best equipped to hold it. The rough math is that the merchant fee funds a loan yielding an APR of 22.8% for the investor (capital provider) while the consumer pays zero interest. This is the Golden Age of Credit™ after all.

Investor Economics: Assume a $100 BNPL loan. $25 is paid upfront by the Consumer, so an Investor pays $73 for a $75 loan, discounted for risk, fees, and return expectations. The Investor receives $75 from customer repayments over 6 weeks minus servicing fees of $0.25. A $1.75 profit on $73 investment over 6 weeks is a 2.4% return, or 22.8% annualized (52 weeks/6 weeks = 8.67 periods each year; annualized return = (1+0.024)8.67 - 1).

For the Economy: This process is another step toward a Complete Market. It converts a financing tool into a discrete financial instrument that can be priced and traded based on the views of financially-motivated participants, i.e. it converts a balance sheet item into a tradeable security. The allocation of capital becomes more efficient as the number of heterogeneous market participants increases via the Wisdom of Crowds. Thus, this over time reduces the costs of credit for consumers and businesses.

BNPL providers have fairly clear terms and retain the flexibility to adjust their own risk. For borrowers:

Late Fees: A modest fee, often capped to keep things reasonable. Alice forgets a $25 installment on her $100 DoorDash transaction, she’s hit with a $7 late fee, tacked onto her next payment. Annoying, but it probably won’t push her down a debt spiral.

Credit Impact: Alice’s credit score takes a hit if the BNPL provider reports it (many don’t for short-term plans). Most BNPL defaults stay off the radar of the credit bureaus, unlike credit card delinquencies, but this is changing.

Account Lockout: BNPL platforms can freeze account her account if it gets over-leveraged and moves into the ‘high-risk borrower’ category.

Collections: If payments stay delinquent for months, providers will escalate to collections.

APRs: Most BNPL plans start at 0% APR for short-term deals, and missing a payment doesn’t change the rates. However, some providers might revoke the 0% rate, slapping a standard rate of, say 20%, on the remaining balance. Late fees mimic interest even if called interest-fee loans.

This is a fair concern, with the data showing that those with lower incomes, lower education, and worse credit (redundancies here) are more likely to use BNPL. Even with adverse selection for BNPL, the underwriting is for each transaction, not for all monthly spending like that in credit cards; so if a consumer misses a payment, the BNPL provider can stop lending immediately, as opposed to the credit card company which has to underwrite the person’s full ability and willingness to repay their debts. This tech-enabled granularity allows for legibility and hence greater precision and predictability. Asking your neighbor to watch your dog for a few days is a much lower bar than asking them to raise your toddler kids if you get hit by a bus because the stakes and duration of your ask are very different. BNPL is granular, precise, and agile. Credit cards are monolithic and inert. See the next section for more on legibility.

In Design, the principle of Universal Design focuses on creating inclusive systems and tools that improve usability for all. Autocorrect, text-to-speech readers, dark mode, and subtitles all came from Universal Design. Similarly, lending that makes credit more affordable and accessible for lower-income individuals will reduce credit costs for all borrowers.

I’m a James C. Scott appreciator. Credit cards account for 63% of all US retail purchases but bundle all sorts of non-discretionary and discretionary purchases together. Your $30 takeout order is bundled with “financing” for a new coffee machine, Uber rides, airline tickets, gym membership, dry cleaning, a tire change, and maybe even your monthly rent. Additionally, your credit card rate is also obscured by complex fee structures, variable interest rates, reward points, hotel points, and airline miles. So it’s hard to precisely price the risk of that $30 loan.

BNPL disentangles these purchases. Each loan is for a specific item, with a fixed repayment schedule over a very short term (usually 6-8 weeks).

Underwriting happens at the point of sale for that specific transaction. Investors buying securities backed by these loans get exposure to a pool of very similar, short-term risks, making it easier to model and understand compared to a portion of a bank's diversified credit card portfolio. The granular control lets providers nip risks in the bud without punishing borrowers into financial destitution. Unlike credit cards, where a few missed payments could balloon to a 5-figure limit, BNPL’s transaction-level underwriting caps the damage. This is legibility in action—providers see exactly what’s gone wrong and adjust.

For investors, defaults are baked into the yield math: the 22.8% annualized return must also account for the burrito deadbeats. This improved legibility means the risk premium that’s embedded in a blended credit card rate can be isolated, traded, and hence compressed.

While defaults happen, the short duration means they won't cascade through and clog up the financial system in the same way longer-term, larger debts like mortgages did during 2006-2008. But even if BNPL scales massively, the risk sits on the balance sheets of credit funds and hedge funds, not deposit-backed banks. This unbundling makes the specific risk of financing everyday consumption more visible and manageable. Banks are already using Significant Risk Transfers to transfer risk to non-bank investors (SRTs move loans’ risks and returns from banks’ balance sheets to credit investors so banks keep the customer relationship while the risks & returns are transferred to investors). Thus, even if the BNPL securitization market grows exponentially, risks will be shifted toward investors who can stomach them, rather than banks dependent on retail deposits. Moral hazard, counterparty risks, etc. etc. remain, but willing buyers are transacting with willing sellers.

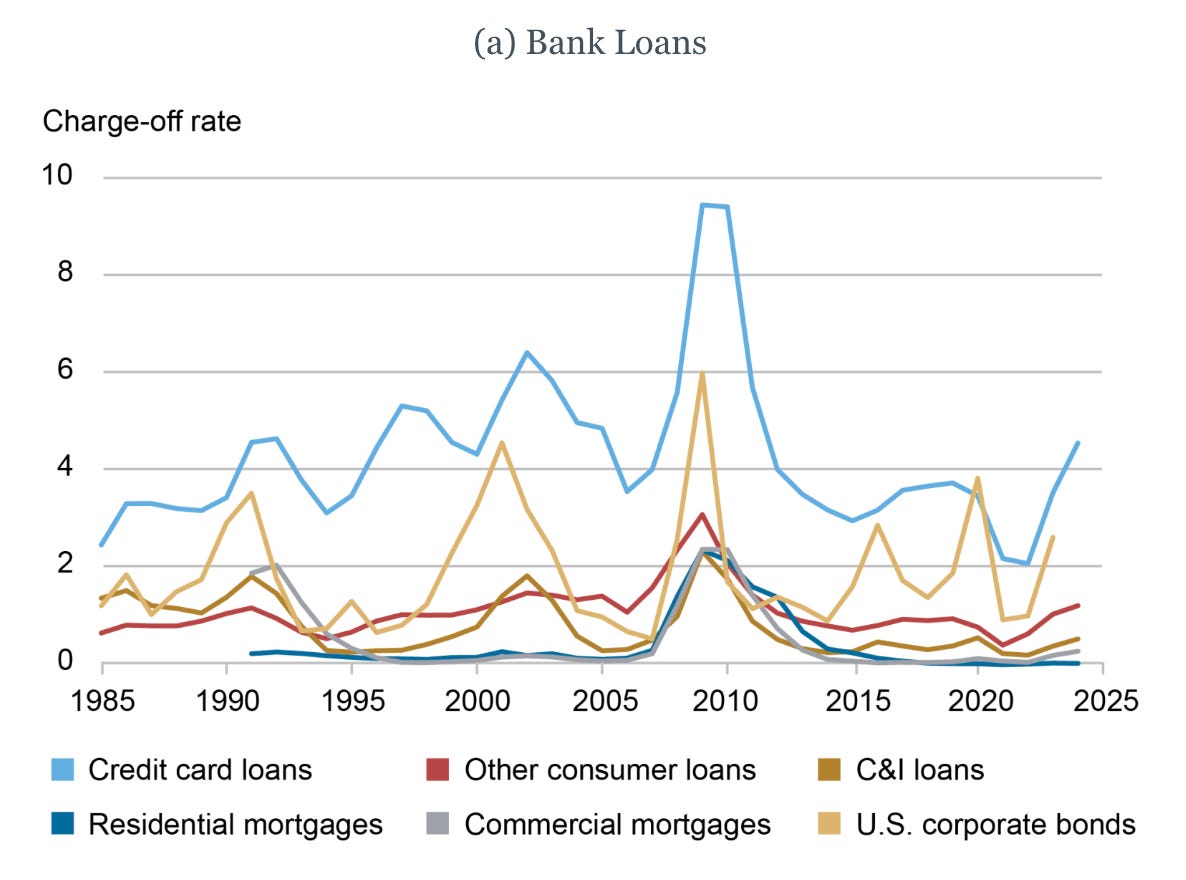

Losses across different FICO score portfolios tend to move together, rising during economic downturns, and currently cannot be diversified within the credit card market. Additionally, credit card losses (charge-off rates) are highly correlated with losses on other types of loans and corporate bonds. Which is to say that credit card lending risks are undiversifiable across other lending markets and therefore banks/investors have to be compensated to hold this risk. Hence, consumers must pay more to borrow because their risk of default cannot be diversified.

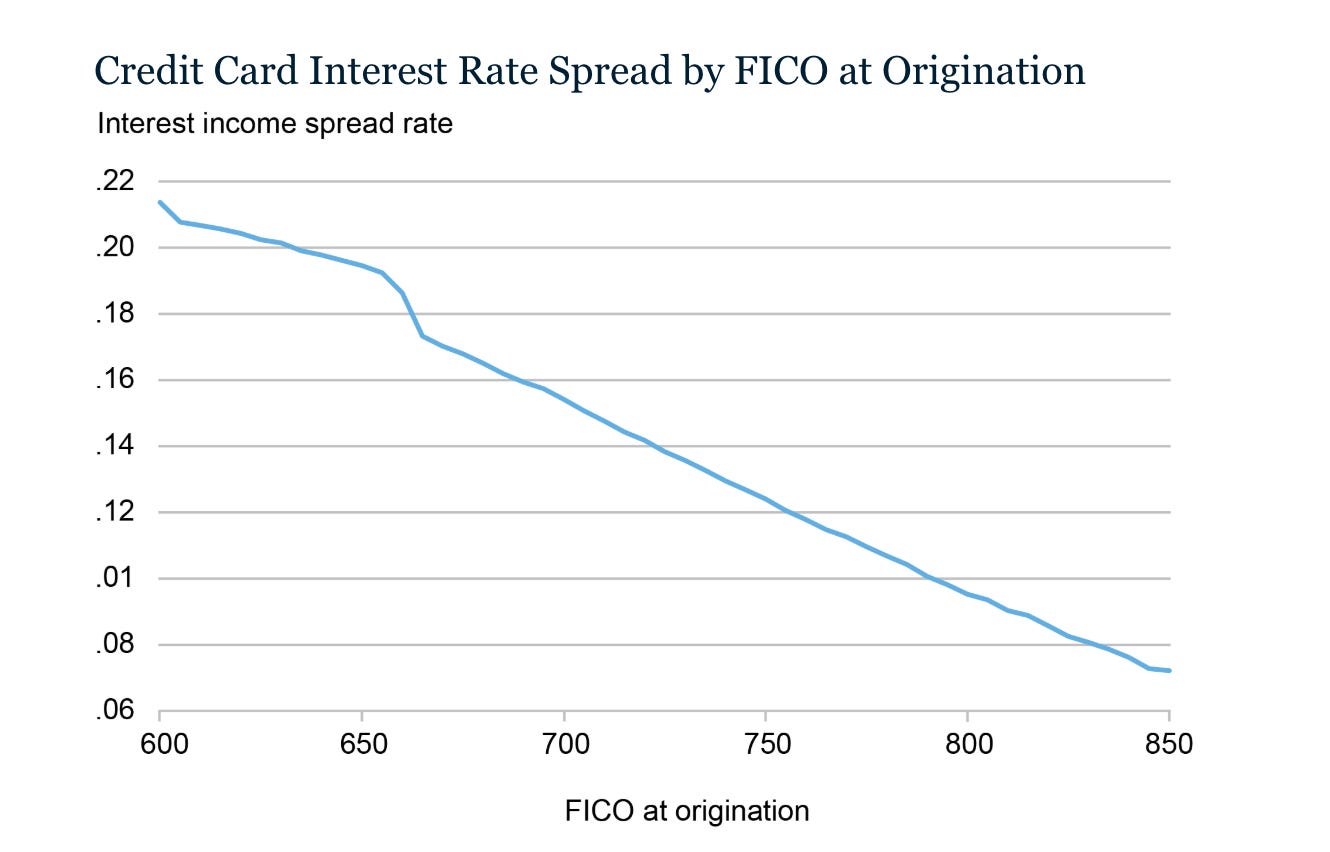

At the moment, for credit cards, the average interest spread over the Fed Funds rate (the risk-free rate) is 14.5%, and ranges from 21% for borrowers with a low FICO score of 600, to 7.22% for those with the highest score of 850. The estimated non-diversifiable risk premium is 5.3% per year, or 37% of the average risk premium of 14.5%, which seems really high. I expect this component of the credit card spread will get compressed as the BNPL securitization market matures.

As the BNPL-Backed Securities (“BBS”) market develops, I expect to see the creation and growth of BBS Indexes and associated derivatives and BBS ratings from the credit ratings agencies. ABS indexes already exist for mortgage-backed securities, CDS indexes for corporate bonds, etc. Investment banks will create futures, options, swaps, etc. so investors can manage their BBS portfolios. If a fund holds a portfolio of BBS and is worried about an increase in takeout BNPL credit losses, they could short the “Food Delivery BBS Index”, and similarly the “Clothing BBS Index”, the “Electronics BBS Index”, and so on.

Do I want to see a Sports Betting BBS Index? No. Will it happen? Definitely. Sports betting does a lot of damage to the finances of American households but when the loans backing them are securitized, they will make for a great fixed income product because because gambling is a somewhat recession-resilient industry, much like other ‘sin sectors’ like alcohol and tobacco (BBS indexes for alcohol and tobacco will also happen, and around here is where I may get tired of winning).

Perhaps, a case can be made for some paternalism i.e. to not increase financing for harmful products. And of course, we should also expect to see a Rental Market BBS Index because BNPL for monthly rent payments is already commonplace.

One argument made is that BNPLs, by extension of credit to people who don’t have traditional credit available, allow customers to overextend themselves. (This is, for social reasons, very rarely articulated as “I am better at math than women who shop at Sephora, think they will not make good choices, and accordingly think they should have less choices presented to them.” But it is that argument.)—Patrick McKenzie

Here is where market completion comes in. An investor can bet on the rental market holding up by buying the Rental Market BBS index futures and selling the broader BBS index if they think rentals will outperform. Similarly, DoorDash can sell the Food Delivery index to protect against a potential drop in their earnings if it sees softening demand. These index prices can serve as a signal and guide lending decisions in the BNPL market and the wider credit market because they will aggregate the opinion of the market’s participants.

When investors can hedge non-diversifiable risks, they require a lower return/yield for taking on that exposure. This translates back through the capital allocation chain, lowering the fees merchants pay, or allowing BNPL providers to offer even better terms i.e. cheaper credit for borrowers, and making the whole economy more efficient at allocating resources. While financial engineering doesn’t eliminate risk; it transfers it to those best equipped to handle it, making credit cheaper and capital allocation more effective.

More speculative but still plausible: by providing flexible, short-term financing with manageable risks, BNPL will make the economy more resilient to recessions by supporting consumption and business stability. BNPL’s short duration and non-systemic risks limit cascading defaults. This flexibility could buffer downturns as consumers & merchants and their financiers adapt more quickly to changing conditions.

This process–underwriting individual loans, securitizing them, and creating indexes and derivatives–is a classic pattern in financial markets. So while “burrito bonds” sound absurd, absurdity is common at the frontiers of innovation.

In this case, tech-enabled financial engineering leads to more efficient credit, granular risk transfer, and deeper markets. And that’s a win.

![[Web dev for beginners] CSS: Learn the essentials quickly](/image/r?src=templates/thedailycurrents.com/v8/images/categories/16.jpg&w=825&h=520&zc=1)

![[Web dev for beginners] CSS: Learn the essentials quickly](/image/r?src=templates/thedailycurrents.com/v8/images/categories/19.jpg&w=825&h=520&zc=1)